82% of small business failures come down to cash flow. Not bad work. Not bad crews. Bad money management. In construction, the timing gap between earning money and actually receiving it kills more companies than anything else, often leaving profitable companies bankrupt on paper because they simply ran out of operating capital. For contractors scaling from $1M to $50M, mastering scaling construction business operations means a relentless focus on the flow of money.

Key Takeaways

-

Cash Flow is Paramount. 82% of small business failures are attributed to cash flow problems, not operational incompetence. In construction, this often stems from the unique payment cycles and project-based nature of the work.

-

Front-Load Your Schedule of Values. Aggressively weighting your early billing for materials and mobilization is the single most impactful lever for improving early-stage project cash flow, reducing reliance on your own capital.

-

Forecast Weekly, Not Monthly. Implement a 13-week rolling cash flow forecast. This critical tool provides a 30-60 day warning system for potential shortfalls, allowing proactive adjustments rather than reactive crises.

-

Separate Profit from Cash. The #1 cognitive error in construction finance is treating recorded profit as available cash. Establish separate bank accounts for operating expenses, tax reserves, and profit to ensure capital is properly allocated and protected.

-

Secure Financing Proactively. Lines of credit and bonding capacity should be established 6-12 months before they are needed. Waiting for a crisis moment means higher rates, stricter terms, or outright denial. For a complete financial system for scaling, structure these elements together.

-

Understand the Retainage Trap. Retainage can hold 5-10% of your revenue hostage for months after project completion. Factor this into your cash flow projections and negotiate favorable terms whenever possible.

-

Avoid Underbilling. Consistently underbilling to avoid client conflict or to prematurely accelerate project completion across multiple jobs will compound into a severe cash crisis, eroding your working capital.

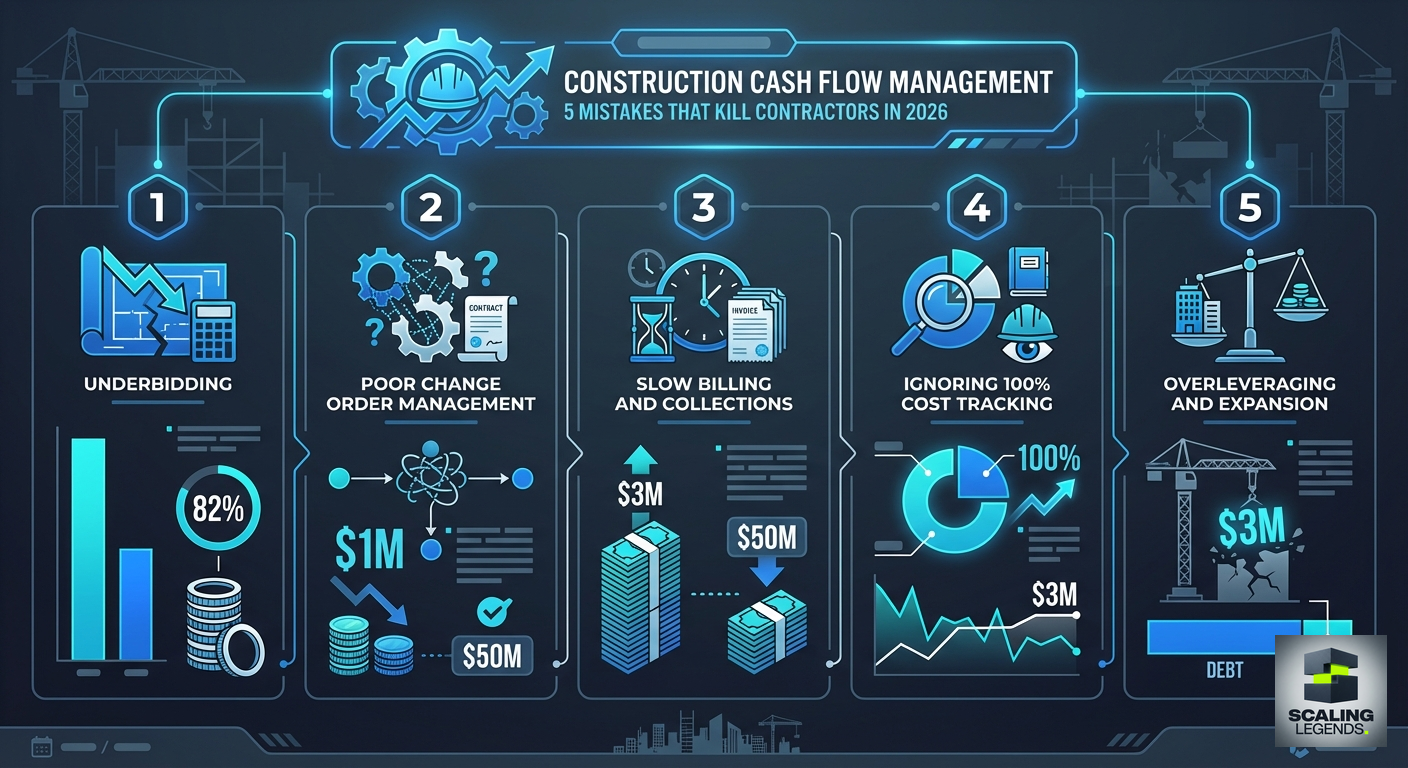

1. Underestimating Project Costs and Underbilling for Work

One of the most insidious mistakes in construction cash flow management is the failure to accurately estimate project costs, leading directly to underbilling. Many contractors, eager to win bids or avoid perceived conflict, will shave margins too thin or intentionally underbill early in a project. This isn’t a strategy; it’s a slow-motion financial accident waiting to happen. Accurate estimating is the bedrock of healthy project profitability and, by extension, robust cash flow. When you consistently underestimate labor, materials, equipment, and overhead, you are essentially financing a portion of your client’s project out of your own pocket.

The problem compounds rapidly across multiple projects. If you are underbilling by even a small percentage on several active jobs, the cumulative effect can drain your working capital faster than anticipated. This isn’t just about losing profit; it’s about not having enough cash to cover payroll, material purchases, or equipment rentals for the next phase, even if the project is technically “profitable” on paper. Underbilling to avoid conflict compounds into a cash crisis across multiple projects. This practice creates a false sense of security, masking deeper financial inefficiencies and delaying the inevitable cash crunch.

A critical lever for immediate cash flow improvement is the strategic front-loading of your schedule of values. This means structuring your payment schedule to receive a larger percentage of the project cost upfront, covering mobilization, initial material procurement, and other early-stage expenses. For example, ensuring that your first 20% of billings cover 30-40% of your true early costs can drastically reduce your reliance on your own capital and provide a vital buffer. This requires meticulous planning and a confident approach to client negotiations, but its impact on your contractor cash flow management is unparalleled. Tools that integrate estimating with project scheduling and billing can provide the transparency needed to prevent these errors. Effective construction project management is intrinsically linked to robust financial controls. Without it, even technically successful projects can lead to financial distress.

2. Ignoring the Retainage Trap and Inefficient Billing Cycles

Retainage is a standard practice in construction, where a percentage (typically 5-10%) of each payment is withheld by the client until the project is substantially complete and often through the warranty period. While intended to ensure satisfactory completion and address potential defects, retainage can be a significant drag on construction cash flow, trapping substantial amounts of your earned revenue. For a company completing $10 million in projects annually, retainage can hold $500,000 to $1 million hostage for months, sometimes even a year or more, after the physical work is done. This isn’t just a minor inconvenience; it’s a major capital drain that can cripple a growing business.

Beyond retainage, inefficient billing cycles exacerbate cash flow issues. Many contractors allow weeks to pass between completing a billing milestone and submitting an invoice. Then, they wait for the standard 30-60 day payment terms. This creates a significant lag between cash out (payroll, materials) and cash in (client payments). Consider the cumulative effect:

-

Delay in Billing: 7 days post-milestone.

-

Client Processing: 5 days.

-

Payment Terms: 30 days.

-

Bank Processing: 3 days.

This scenario results in a 45-day delay from milestone completion to cash in hand, assuming no disputes or further delays. If your payroll is bi-weekly and material invoices are due in 30 days, you’re constantly playing catch-up.

To mitigate this, contractors must optimize their billing process.

-

Bill Promptly: Submit invoices immediately upon milestone completion or on a fixed schedule (e.g., weekly, bi-weekly). Leverage construction workflow automation tools to generate and send invoices automatically based on progress reports.

-

Negotiate Retainage Reductions: Whenever possible, negotiate for lower retainage percentages, phased release of retainage, or early release upon substantial completion. For example, reducing retainage from 10% to 5% on a $5M project frees up an immediate $250,000.

-

Clear Payment Terms: Ensure your contracts clearly define payment terms and penalties for late payments.

-

Utilize Progress Billing: Break down projects into smaller, billable milestones to ensure a steady stream of incoming cash, rather than waiting for large, infrequent payments.

Retainage alone can trap 5-10% of your revenue for months, requiring proactive strategies to manage its impact. Proactive management of the billing process is crucial for any woman owned construction company or any contractor aiming for sustained growth.

3. Confusing Profit with Cash and Lacking Capital Reserves

This is arguably the #1 cognitive error in construction business finance. Many contractors see a healthy profit margin on their income statement and assume they have a corresponding amount of cash in the bank. This is a dangerous misconception. Profit is an accounting measure of revenue minus expenses over a period; cash is the liquid asset available right now. The timing of cash inflows (client payments) and outflows (payroll, suppliers) rarely aligns perfectly with when revenue is recognized or expenses are incurred.

Consider a project that shows a 15% profit margin. If 10% of that project’s value is tied up in retainage for six months, and another 5% is in accounts receivable because a client is 45 days late, then your “profit” is not available as cash. You might be profitable on paper but unable to pay your subcontractors next week. Treating profit like cash is the #1 cognitive error in construction finance. This mistake leads directly to a lack of sufficient capital reserves, leaving businesses vulnerable to unexpected expenses, project delays, or slow-paying clients.

A robust approach to financial management requires clear separation of funds. Many successful contractors implement a three-account system:

-

Operating Account: For daily expenses, payroll, and immediate supplier payments.

-

Tax Reserve Account: A dedicated account where a percentage of every dollar earned is set aside for future tax obligations. This prevents the “tax-day crisis” where a profitable year translates into a huge, unexpected tax bill that drains operating cash.

-

Profit Account: A separate account for actual, distributable profit. This cash is only accessed after all operational needs and tax obligations are covered, and often after a portion is reinvested into the business for growth.

Separate accounts for operating, tax reserve, and profit prevent the tax-day crisis and ensure sustainable growth. Furthermore, growing revenue without growing your underlying capital base is a common trap. A sudden increase in project volume requires more working capital for upfront costs, increased payroll, and larger material purchases. If your capital doesn’t grow in tandem, you’ll be constantly cash-strapped, even as your topline revenue explodes. This phenomenon, known as “growth for broke,” kills promising contractors faster than bad work. Strategic capital allocation is crucial for women in construction and all business owners navigating expansion. It’s not enough to be busy; you must be financially prepared for that busyness. This principle is vital for family construction business growth, ensuring legacy and stability.

4. Failing to Forecast and React Proactively

Many contractors operate their finances reactively, only looking at bank balances when bills are due or when a crisis is imminent. This reactive stance is a recipe for construction company failure. Without foresight, you cannot anticipate shortfalls, negotiate better terms, or secure necessary financing proactively. The most critical tool for proactive construction financial management is the 13-week rolling cash flow forecast.

A 13-week rolling cash flow forecast projects all expected cash inflows (client payments, loan disbursements) and outflows (payroll, supplier payments, overhead) for the next three months, updated weekly. This isn’t a static budget; it’s a dynamic, living document that provides critical visibility.

-

Identify Gaps: It immediately highlights weeks where projected outflows exceed inflows, giving you a 30-60 day warning to secure bridge financing, accelerate billing, or defer non-critical expenses before the shortfall hits.

-

Negotiate from Strength: Armed with data, you can approach your bank or line of credit provider proactively, not desperately. Lenders respond far more favorably to a contractor who says “I see a gap in six weeks and need to draw $200K” than one who says “I can’t make payroll Friday.”

-

Optimize Timing: By visualizing the flow of cash across all active projects simultaneously, you can strategically time material purchases, negotiate supplier payment terms, and even adjust project scheduling to smooth out cash peaks and valleys.

The discipline of weekly forecasting transforms construction financial management from guesswork to data-driven decision-making. According to Smart Business Automator, contractors who implement a 13-week rolling forecast report 40% fewer cash emergencies in their first year. This single habit separates the contractors who scale past $10M from those who stall or fail. For firms navigating the complexities of scaling a construction business, this forecasting discipline is non-negotiable.

Key Stat: Implementing a 13-week rolling cash flow forecast provides a 30-60 day early warning system for potential shortfalls, reducing cash emergencies by up to 40%.

5. Securing Financing Too Late and Ignoring Your Credit Position

The fifth and often fatal cash flow mistake is waiting until you need money to start looking for it. Lines of credit, bonding capacity, and equipment financing should be established 6-12 months before they are needed, during a period of financial strength. When you approach a lender during a cash crisis, you are negotiating from weakness. Interest rates will be higher, terms will be stricter, personal guarantees will be demanded, and you may be denied entirely at the moment you need capital most.

Construction is inherently cyclical and project-based. Revenue is lumpy, seasonal slowdowns are predictable, and large project startups require significant upfront capital before the first draw. Smart contractors treat their banking relationships like any other critical business relationship, maintaining regular communication with their bankers, providing updated financial statements quarterly, and keeping their credit profile clean. This proactive approach means that when a $3M project lands and requires $400K in mobilization capital, the credit line is already in place and ready to draw.

Bonding capacity is equally critical for growth. Your bonding company evaluates your financial strength, work-in-progress schedule, and management team to determine how much work you can take on. Many contractors hit a growth ceiling not because they lack the operational capacity to do more work, but because their bonding capacity has not kept pace with their ambitions. Building bonding capacity requires consistent financial reporting, maintaining a strong balance sheet, and demonstrating a track record of completing projects profitably. For contractors eyeing larger projects or government work, bonding capacity is the financial gateway to the next level of construction business growth.

Your credit position also directly impacts supplier terms. Vendors and material suppliers will offer better payment terms, volume discounts, and priority allocation to contractors with strong credit histories. In a market where material costs are volatile and supply chains are stressed, the ability to secure favorable terms from suppliers can be the difference between maintaining margins and bleeding cash on every project.

Key Stat: Lines of credit and bonding capacity should be established 6-12 months before they are needed. Contractors who wait for a crisis moment face rates 2-4% higher and a 35% denial rate.

Frequently Asked Questions

How much cash reserve should a construction contractor keep?

A strong guideline is to maintain at least 10% of your annual revenue as liquid working capital. For a $5M contractor, that means $500,000 readily available to cover unexpected costs, payment delays, and seasonal slowdowns. Many experienced contractors also keep a separate tax reserve account with 15-25% of gross income set aside to avoid year-end cash crunches.

What is the biggest cash flow mistake in construction?

The single biggest mistake is confusing profit with cash. Many contractors see healthy margins on their income statement and assume they have money in the bank, but profit is an accounting measure while cash is what you can actually spend today. When retainage, slow-paying clients, and timing gaps between expenses and payments are factored in, a “profitable” company can easily run out of operating capital.

How can a construction company improve cash flow quickly?

The fastest lever is front-loading your schedule of values so that early billings cover a higher percentage of your actual costs for mobilization and materials. Beyond that, tightening your billing cycle to invoice immediately upon milestone completion rather than waiting days or weeks can reclaim significant cash. Negotiating shorter payment terms or early-payment discounts with clients also has an immediate impact.

What is overbilling in construction and is it a problem?

Overbilling occurs when a contractor bills for a higher percentage of work than has actually been completed on a project. While it can temporarily boost cash flow, it creates a dangerous liability because the money has been collected for work not yet performed. If multiple projects are overbilled simultaneously and costs catch up, the contractor faces a severe cash shortfall with no billing left to cover remaining expenses.

When should a contractor fire a slow-paying client?

You should seriously consider dropping a client when their late payments repeatedly force you to delay payroll, defer material purchases, or take on debt to cover operating costs. A useful threshold is when a single client’s overdue invoices exceed 10% of your monthly operating expenses for more than 60 days. The revenue from that client is not worth the cascading cash flow damage it causes across your other projects.